SEEING THE POTENTIAL FOR AN INDUSTRY

A network can be a powerful way to give a new idea traction as it moves to gain widespread support. That was exactly the situation with the concept of impact investing. By 2007, a variety of financial innovators had developed approaches to socially-conscious investment and were paving the way for new avenues to direct capital for social good. For instance, Jacqueline Novogratz started the nonprofit Acumen Fund to invest in social enterprises in East Africa and South Asia. Muhammad Yunus had established the Grameen Bank to lend to lower-income women in Bangladesh. Willy Foote founded the nonprofit Root Capital to lend to farmer cooperatives throughout Latin America and Africa. These and many other organizations offered a wide range of avenues for satisfying the growing demand for investment that sought some combination of financial and social outcomes. And as is typical for a field in its formative stage, there was a range of terms to describe this activity, each with its own meaning and nuance: socially responsible investing, blended value, mission-driven investing, and so on. And while there was a great deal of effort to develop various niche models, there was no infrastructure that would enable the market to grow as a whole.

This fragmentation struck Antony Bugg-Levine when he joined The Rockefeller Foundation in 2007 and was asked by the Foundation’s President, Judith Rodin, to evaluate its impact investing portfolio. In the book Impact Investing, he and his co-author Jed Emerson describe what they saw at the time: the need to set the rules and create a worldwide playing field, which would necessitate transformation across capital markets, performance measurement, and public policy. It was clear that no individual, however charismatic, would be able to create these transformations alone. As they wrote, “It will be an especially tricky transition since it requires a focus on the “we” of sustained social change, not just the “me” of social entrepreneurship… A single-minded focus on individuals obscures the crucial role collaboration and coordination need to play in impact investing’s next phase. Impact investing will take off when its pioneers and newcomers collaborate effectively, building the infrastructure that will enable the next wave of talent and capital to join the field… In [this] emerging phase, the impact investing industry suffers from fragmentation with an increasingly crowded field of subscale players unable to rise above the noise.”

ASSEMBLING A NETWORK

What Bugg-Levine saw in this situation were many of the elements that make it a natural choice to build a network. Investment had tremendous potential to provide capital for social problem-solving, but that potential wouldn’t be realized unless the many disconnected innovators began to act like they were building the same field. Bugg-Levine made the case that The Rockefeller Foundation should launch an initiative with the goal of accelerating this change in behavior, and the Board of Directors agreed. “We believed that people needed to interact in unusual constellations,” he reflected in a recent interview. “Institutional investors needed to be in closer contact with philanthropists, and that philanthropists needed to be in closer contact with entrepreneurs, and we believed that cross-fertilization would create action. We wanted people to come together who hadn’t seen themselves as part of the same movement. The goal was to create a ‘rhetorical umbrella’ under which many people could huddle.”

The first step of this new initiative was to test the attractiveness of this idea with a sampling of the various actors working in the market, which Bugg-Levine did by holding a convening in the summer of 2007 at the Foundation’s retreat center in Bellagio. “We asked, do you think there would be utility in your silos working together?” he recalls. By posing that question, he focused the group’s attention on what lies at the core of a network’s viability: whether there is common ground for the network to work together. At this early stage, it was important for the funder to be able to judge when to ask that question, and how best to show a group the potential for collective work. Bugg-Levine used this convening to ask the question, and fortunately the answer was yes. The participants were able to identify initial categories of work that they wanted to pursue together, created informal working groups, settled on a name (the Rockefeller Impact Investing Collaborative) that was the first use of “impact investing” to describe the market, and agreed to continue their work at another convening in nine months’ time. With that first fuzzy definition of the common ground in place, the work of the network began. Working with Monitor Institute, Bugg-Levine followed through with a second convening in 2008 that gathered an expanded group of 40 participants, representing a wider swath of the marketplace.

It was at this second convening that both The Rockefeller Foundation and the participants were able to see a clear path forward for this nascent industry to solve social and environmental challenges with greater efficiency. The group aligned around the overarching goal of moving beyond uncoordinated innovation to a focus on market-building and expressed considerable enthusiasm for advancing its work through four formal working groups, each of which took on a separate topic: creating of a global network of leading impact investors, developing a standardized framework for assessing social and environmental impact, starting an impact investing bank, and developing a working group of investors focused on sustainable agriculture in sub-Saharan Africa.

SCALING UP AND CREATING A BACKBONE

Part of the art of engaging with a network is in spotting when it is at an inflection point, and judging the best next step from the perspective of the group rather than your own goals. As Bugg-Levine reflected, “When a foundation calls you to a meeting, you’ll show up whether you think it is a good investment of your time or not. As a program officer, it’s very easy to convince yourself that you’ve identified a network with a lot of interest. You have to ask, how do I know if this network is necessary?” Yet he felt confident at this point that the network was ready for growth. One strong indicator for him was the energy of the 2008 convening, and another was the constant demand for him and his small team to play the role of network weaver, making introductions and spreading information, which had grown into an intensive task.

The first step that The Rockefeller Foundation took in scaling the network was to develop a clear vision for the field that reflected the views of the network’s current participants. This was important in order to accomplish several goals: anchoring the dialogue in the existing history and research, capturing the insights of the 2008 convening, reflecting back the conversation to help cement the understanding and motivation of the 40 people involved. He was able to do that by providing lead funding for Monitor Institute to create Investing for Social and Environmental Impact: A Design for Catalyzing an Emerging Industry. That research began in 2008, informed the dialogue and framed key questions at the 2008 convening, used the convening’s conversations to refine the thinking, and was released in January 2009. This enabled the Foundation and the report’s other funders—the Annie E. Casey Foundation, W.K. Kellogg Foundation and JPMorgan Chase Foundation—to spread the word about the importance of building a market in the words of the market’s own leaders.

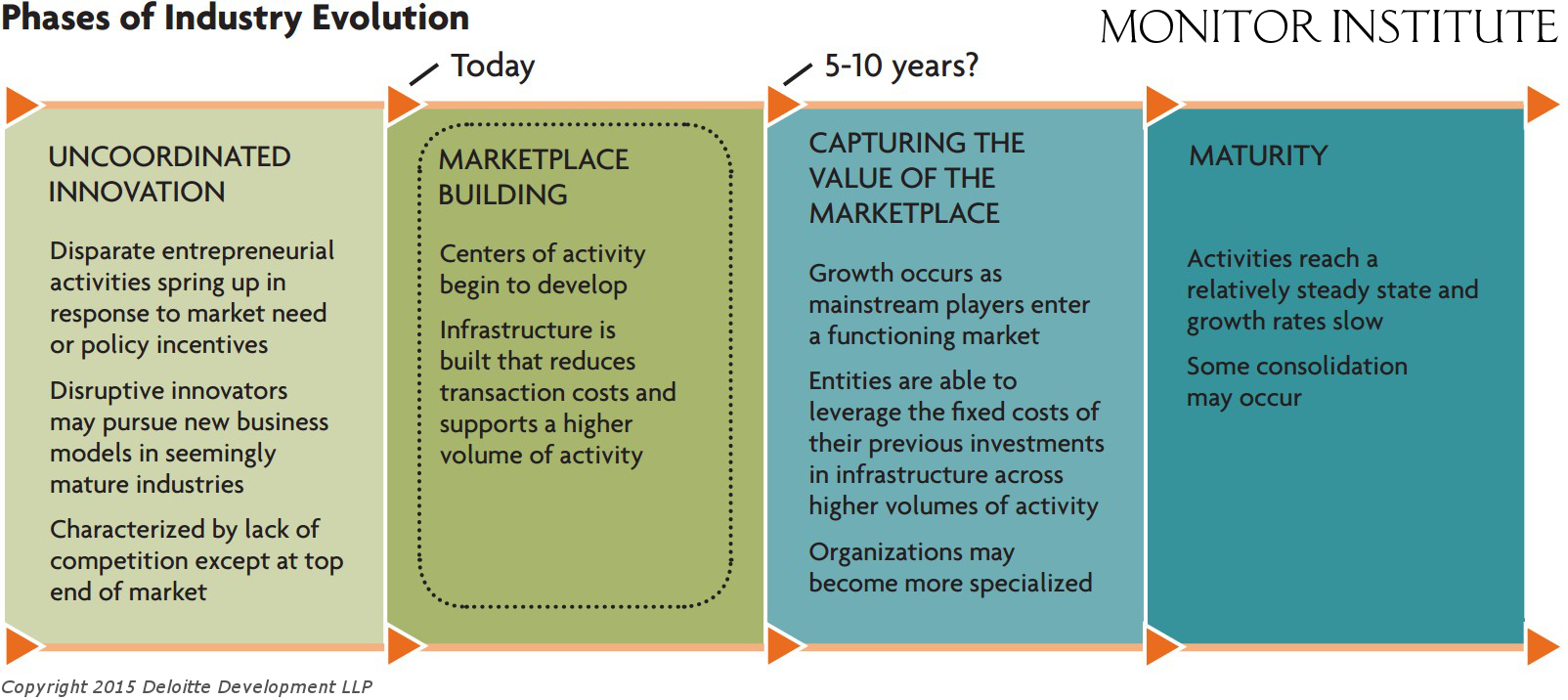

One of the frameworks that emerged in that report was a succinct description of the developmental path that is typical for any new market as it becomes established. Markets typically undergo a period of uncoordinated innovation before they enter a phase of marketplace building, which in turn sets the stage for achieving the initial vision—capturing the value of the marketplace and finally maturity. Understanding that process was a helpful realization for both the funders and the network’s participants, and it can be equally helpful for the actors involved in other early-stage markets where networks are forming. That process is described in more detail in this visual:

The second step that The Rockefeller Foundation took to scale up the network was to establish a new nonprofit that could house the network’s backbone functions. It simply wasn’t sustainable for Bugg-Levine and his team to continue weaving the network and playing a variety of other backbone roles themselves, particularly as the report attracted attention to the network’s vision. In his words, “The longer we held on to [the network], the more likely we were to stunt its growth.” Starting a stand-alone organization wasn’t seen as the ideal solution, but none of the participants were well-positioned to play backbone roles themselves, since there were meaningful financial outcomes at stake and each would have their own conflicts of interest.

In taking both of these steps, The Rockefeller Foundation faced important choices about the use of its brand. Scaling up meant that this initiative had to transition from an effort led by the Foundation to an effort led and owned by its participants, and supported by a larger group of funders. That logic justified the Foundation playing a behind-the-scenes role, making its involvement as invisible as possible and elevating the role of the network’s participants. But there was also a powerful attraction to the prospect of using the Foundation’s name as a way to attract attention to the effort and lend it credibility. In the case of the report, the Foundation opted to be the lead funder, recruit several other foundations as fellow supporters, and have the document branded by Monitor Institute. In the case of the nonprofit, the Foundation also chose not to use the Rockefeller name, branding it the Global Impact Investing Network (GIIN). The GIIN launched in 2009, nearly a year after the 2008 convening, with the goal of advancing the same four workstreams that the convening participants agreed to pursue.

SHIFTING INTO A NEW SET OF ROLES

The heart of a funder’s decision to engage with a network is the choice of what backbone roles to play, and with the founding of the GIIN, the Rockefeller Foundation both launched the network into a new phase and began playing a different set of roles. Since the GIIN had its own leadership and staff, Bugg-Levine and his team could step out of their position as the principal network-weavers, with Bugg-Levine becoming a member of the new organization’s Board of Directors. The Foundation’s principal investment in the network became not its staff time but its grant dollars, which at first were provided on one-year cycles while the organization established itself.

Over time, the Foundation has also found other ways to build its relationship with the young entity. Program officers have contracted with GIIN staff to make use of their topical expertise, the Foundation has begun requiring the investees of its Program Related Investments program to file reports using metrics that comply with the GIIN’s IRIS standard, and the Foundation has made use of the GIIN’s Investor’s Council to build relationships with like-minded investors.

The past four years have seen yet another shift in the Foundation’s role, as it has wound down its involvement but continued to use its resources and brand to support the network. The impact investing initiative was originally scheduled to end in 2011, but when Bugg-Levine left the Foundation that year to lead the Nonprofit Finance Fund, the Foundation chose to extend the initiative and its core-support grant funding for the GIIN by another two years. At the same time, the Foundation’s President Judith Rodin joined Bugg-Levine on the GIIN’s Board. These moves provided material support, personal engagement, and also reinforced the GIIN’s public credibility. As of 2013, the Foundation formally closed its impact investing initiative, but Rodin continued serving on the Board, and the Foundation allowed the GIIN to use its existing core support funding over a longer period of time.

Looking back, Bugg-Levine believes that timing and persistence were key to the Foundation’s successful cultivation of the network. “We hit a nerve at the right point, and were tireless in pursuing it,” he said. “It has been incredibly rewarding to promote this idea. I remember how excited we were when an obscure blogger first used the term “impact investing,” and now look how far we’ve come, with President Obama and the Pope having discussed it in the same week.”

BY COMPARISON: THE NETWORK’S DESIGN

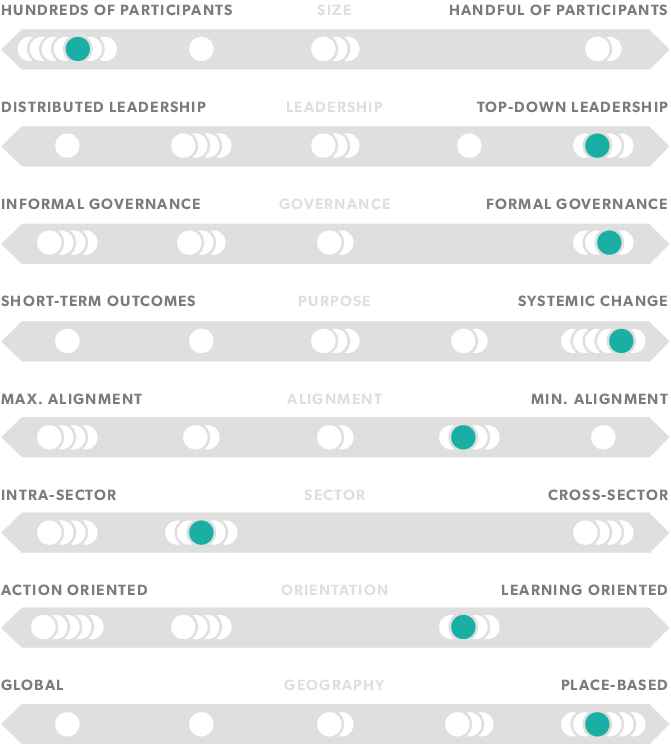

In the section What network design would be most useful? we introduce a simple framework for comparing the ‘design’ of a network — eight basic variables that define its shape and size. See below for our estimation of the design of the Global Impact Investing Network (in teal) versus that of the other networks we profile (in white):

Sources: The Global Impact Investing Network website, a Monitor Institute interview with Antony Bugg-Levine (former Managing Director at The Rockefeller Foundation) in November 2014, a Monitor Institute interview with Brinda Ganguly (Associate Director of Impact Investing at The Rockefeller Foundation) in October 2014, the 2011 book Impact Investing: Transforming How We Make Money While Making a Difference by Antony Bugg-Levine and Jed Emerson (Kindle locations 2703-2743), and the 2009 Monitor Institute report Investing for Social and Environmental Impact: A Design for Catalyzing an Emerging Industry.